CLOUGH GLOBAL ALLOCATION FUND

CLOUGH GLOBAL EQUITY FUND

CLOUGH GLOBAL OPPORTUNITIES FUND

(each a “Fund,” and collectively, the “Fund”“Funds”)

1290 Broadway, Suite 1100

Denver, ColoradoCO 80203

NOTICE OF JOINT ANNUAL MEETING OF SHAREHOLDERS

June 17, 2016

To the Shareholders of the Fund:Funds:

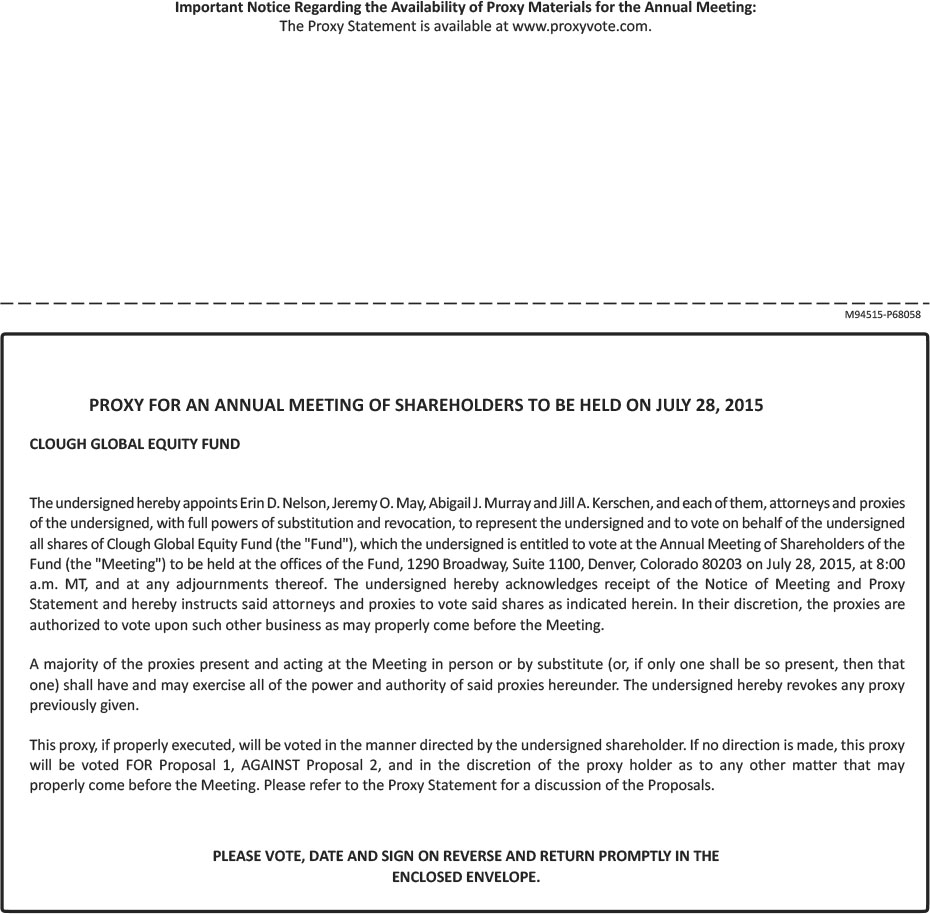

Notice is hereby given that the Joint Annual Meeting of Shareholders (the “Meeting”) of the FundFunds will be held at the offices of the Fund, 1290 Broadway, Suite 1100, Denver, ColoradoCO 80203, on Tuesday, July 28, 2015,20, 2016 at 8:00 a.m. Mountain Time,(Mountain time), for the following purposes:purposes of considering and voting upon the following:

4. The transaction of such other business as may properly come before the Meeting or any adjournments thereof. |

These items are discussed in greater detail in the attached Proxy Statement.

The close of business on May 29, 2015,23, 2016 has been fixed as the record date for the determination of shareholders entitled to a notice of and to vote at the Meeting and any adjournments thereof.

YOUR VOTE IS IMPORTANT REGARDLESS OF THE SIZE OF YOUR HOLDINGS IN THEA FUND. WHETHER OR NOT YOU PLAN TO ATTEND THE MEETING, WE ASK THAT YOU PLEASE VOTE VIA THE INTERNET, BY PHONE OR COMPLETE AND SIGN THE ENCLOSED PROXY CARD AND RETURN IT PROMPTLY IN THE ENCLOSED ENVELOPE, WHICH NEEDS NO POSTAGE IF MAILED IN THE UNITED STATES.

By Order of the Board of Trustees of: | ||

| Clough Global Allocation Fund | ||

| Clough Global Equity Fund | ||

| Clough Global Opportunities Fund | ||

| ||

| Edmund J. Burke | |

[INTENTIONALLY LEFT BLANK]

CLOUGH GLOBAL ALLOCATION FUND (“GLV”)

CLOUGH GLOBAL EQUITY FUND (“GLQ”)

CLOUGH GLOBAL OPPORTUNITIES FUND (“GLO”)

(Each a “Fund” and collectively, the “Fund”“Funds”)

JOINT ANNUAL MEETING OF SHAREHOLDERS

To be Held on July 28, 201520, 2016

PROXY STATEMENT

This Proxy Statement is furnished in connection with the solicitation of proxies by the Board of Trustees of the Fund (the “Board”)Funds for use at the Joint Annual Meeting of Shareholders of the FundFunds (the “Meeting”“Meeting”) to be held on Tuesday,Wednesday, July 28, 2015,20, 2016, at 8:00 a.m. Mountain Time, at the offices of the Fund, 1290 Broadway, Suite 1100, Denver, ColoradoCO 80203, and at any adjournments thereof. The purpose of the Meeting is to consider and act upon the following proposals:

This Proxy Statement is first being sent to shareholders on or about June 30, 2015.20, 2016.

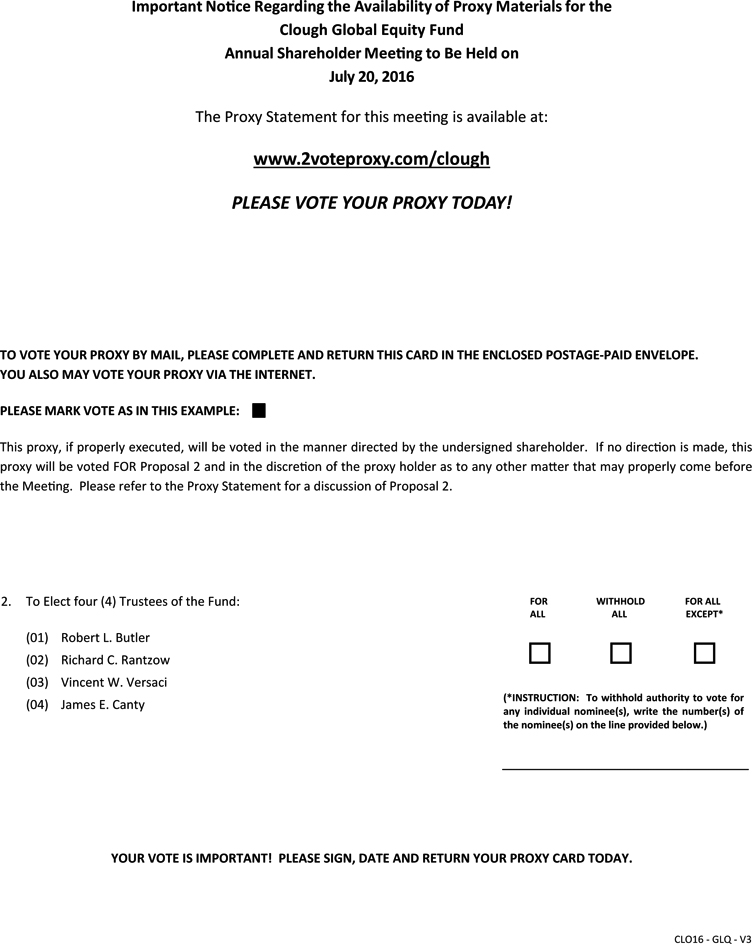

Important Notice Regarding the Availability of Proxy Materials for the Shareholder Meeting to be held on July 20, 2016: Each Fund’s Proxy Statement is available at www.2voteproxy.com/clough.

The Funds’ most recent annual report, including audited financial statements for the fiscal year ended October 31, 2015, is available upon request, without charge, by writing to the Funds at c/o ALPS Fund invites you to attendServices, Inc., 1290 Broadway, Suite 1100, Denver, CO 80203, by calling the Meeting in person. However, whetherFunds at 1.877.256.8445, or not you are personally present, your vote is very important. The Fund offers multiple options for voting your common shares of the Fund (“Common Shares”). You may complete, sign, and date the enclosed proxy card and return it in the postage-paid envelope, vote your shares electronically via the Internet by using the Internet address on the proxy card, or vote by telephone using the toll-free number on the proxy card. Authorizing a proxy will ensure that your vote is counted, even if you cannot attend the Meeting and vote in person.internet at www.cloughglobal.com.

If the enclosed proxy card is properly executed has voting instructions marked, and is returned in time to be voted at the Meeting, the Common Shares represented thereby will be voted as instructed. If you return the properly executed proxy card but give no instruction, then the Common Shares represented thereby will be voted “FOR” Proposal 1 and “AGAINST” Proposal 2, asthe proposal listed in the accompanying Notice, of Annual Meeting of Shareholders. In either case, Common Shares will be votedunless instructions to the contrary are marked thereon, and in the discretion of the proxy holders as to the transaction of any other business that may properly come before the Meeting. Any shareholder who has given a proxy has the right to revoke it at any time prior to its exercise either by attending the Meeting and voting his or her Common Sharesshares in person or by submitting a letter of revocation or a later-dated proxy to thea Fund at the above address prior to the date of the Meeting. You may call 877-256-8445 for information on how to obtain directions to attend the Meeting in person.

1

The close of business on May 29, 2015,23, 2016, has been fixed as the “Record Date” for the determination of shareholders entitled to notice of and to vote at theeach Fund’s Meeting and all adjournments thereof.

| Name & Address | Percentage of Common Shares Held | Total Common Shares Owned | ||

Advisors Asset Management, Inc. 18925 Base Camp Road Monument, Colorado 80132 | 7.76% | 1,385,134 | ||

Bulldog Investors LLC 80 Park West Plaza Two 250 Pehle Ave., Suite 708 Saddle Brook, New Jersey 07663 | 6.58% | 1,171,843 |

In order that your Common Shares may be represented at the Meeting, you are requested to vote on the following matters:

ELECTION OF NOMINEES

TO THEEACH FUND’S BOARD OF TRUSTEES

Nominees for GLV’s Board of Trustees

Listed below are the nominees for the Fund, whoFund. Each nominee is currently a Trustee of the Fund. Mr. Mee, Mr. Versaci and Mr. Burke have each been nominated by the Board for election to serve a three-year term to expire at the Fund’s 20182019 Annual Meeting of Shareholders, or if later, until their successors aresuch Trustee’s successor is duly elected and qualified.

| Proposal | Class | Expiration of Term if Elected |

| Independent Trustee/Nominee | ||

| John F. Mee | Class III | 2019 Annual Meeting |

| Vincent W. Versaci | Class III | 2019 Annual Meeting |

| Interested Trustee/Nominee | ||

| Edmund J. Burke | Class III | 2019 Annual Meeting |

Unless authority is withheld, it is the intention of the persons named in the proxy to vote the proxy “FOR” the election of the nomineeseach nominee named above. Each nominee has indicated that he has consented to be named in this Proxy and to serve as a Trustee if elected at the Meeting. If a designated nominee declines or otherwise becomes unavailable for election;election, however, the proxy confers discretionary power on the persons named therein to vote in favor of a substitute nominee or nominees.

2

Nominees for GLQ’s Board of Trustees

Listed below are the nominees for the Fund. Each nominee is currently a Trustee of the Fund. Mr. Butler, Mr. Rantzow and Mr. Canty have each been nominated by the Board for election to a three-year term to expire at the Fund’s 2019 Annual Meeting of Shareholders, or if later, until such Trustee’s successor is duly elected and qualified. Mr. Versaci has been nominated by the Board for election to a one-year term to expire at the Fund’s 2017 Annual Meeting of Shareholders, or if later, until such Trustee’s successor is duly elected and qualified.

| Proposal | Class | Expiration of Term if Elected |

| Independent Trustee/Nominee | ||

| Robert L. Butler | Class II | 2019 Annual Meeting |

| Richard Rantzow | Class II | 2019 Annual Meeting |

| Vincent W. Versaci | Class III | 2017 Annual Meeting |

| Interested Trustee/Nominee | ||

| James E. Canty | Class II | 2019 Annual Meeting |

Unless authority is withheld, it is the intention of the persons named in the proxy to vote the proxy “FOR” the election of each nominee named above. Each nominee has indicated that he has consented to serve as a Trustee if elected at the Meeting. If a designated nominee declines or otherwise becomes unavailable for election, however, the proxy confers discretionary power on the persons named therein to vote in favor of a substitute nominee or nominees.

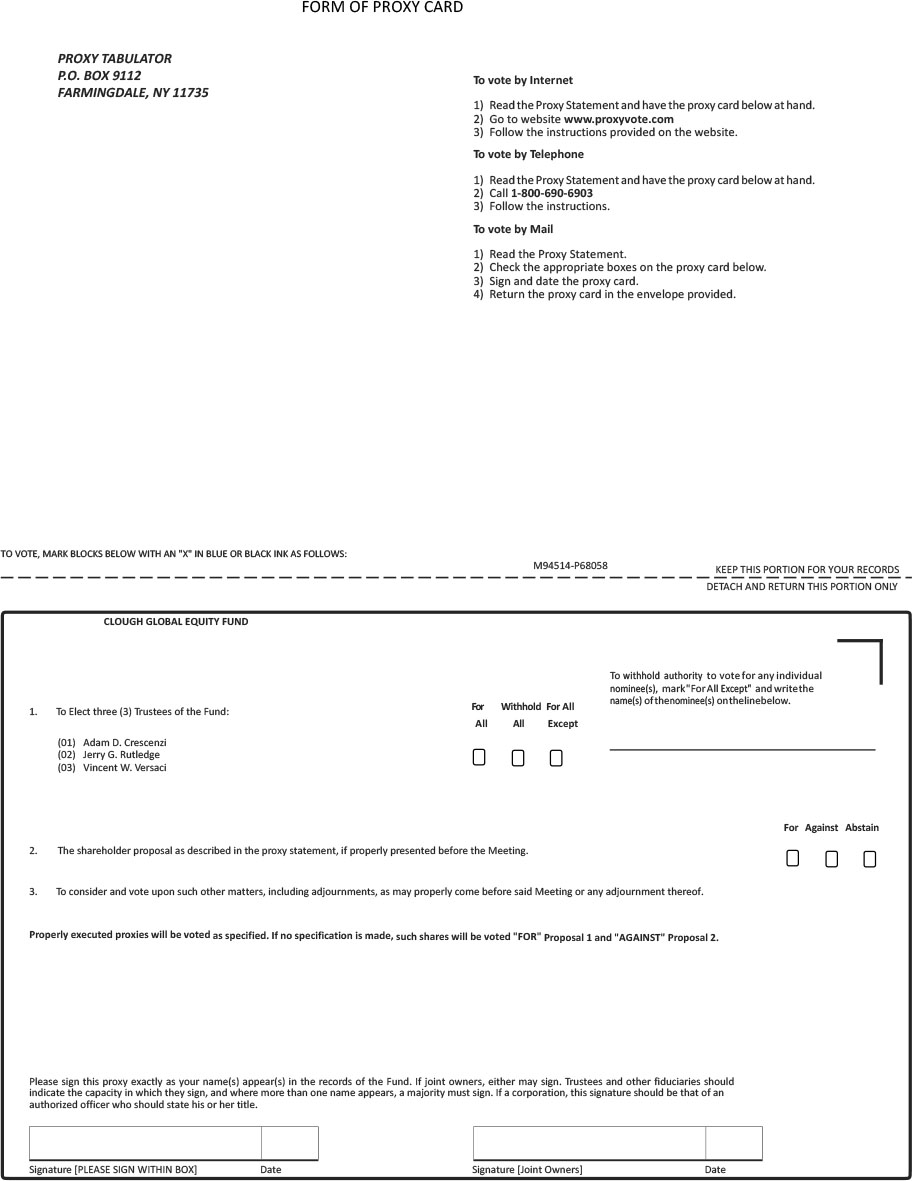

Nominees for GLO’s Board of Trustees

Listed below are the nominees for the Fund. Each nominee is currently a Trustee of the Fund. Mr. Crescenzi and Mr. Rutledge have each been nominated by the Board for election to a three-year term to expire at the Fund’s 2019 Annual Meeting of Shareholders, or if later, until such Trustee’s successor is duly elected and qualified. Mr. Versaci has been nominated by the Board for election to a two-year term to expire at the Fund’s 2018 Annual Meeting of Shareholders, or if later, until such Trustee’s successor is duly elected and qualified.

| Proposal | Class | Expiration of Term if Elected |

| Independent Trustee/Nominee | ||

| Adam D. Crescenzi | Class I | 2019 Annual Meeting |

| Jerry G. Rutledge | Class I | 2019 Annual Meeting |

| Vincent W. Versaci | Class III | 2018 Annual Meeting |

Unless authority is withheld, it is the intention of the persons named in the proxy to vote the proxy “FOR” the election of each nominee named above. Each nominee has indicated that he has consented to serve as a Trustee if elected at the Meeting. If a designated nominee declines or otherwise becomes unavailable for election, however, the proxy confers discretionary power on the persons named therein to vote in favor of a substitute nominee or nominees.

3

Information About Each Nominee’s/Trustee’sabout each Trustee’s Professional Experience Andand Qualifications

Provided below is a brief summary of the specific experience, qualifications, attributes or skills for each Trustee that warranted his consideration as a Trustee/Nominee to the Board of theeach Fund, which isare structured as anindividual investment companycompanies under the Investment Company Act of 1940, as amended (“1940 Act”).

Robert L. Butler– Mr. Butler is currently an independent consultant for businesses. Mr. Butler was President of Pioneer Funds Distributor, Inc. from 1989 to 1998. He was Senior Vice-President from 1985 to 1988 and Executive Vice-President and Director from 1988 to 1999 of the Pioneer Group, Inc. While at the Pioneer Group, Inc. until his retirement in 1999, Mr. Butler was a Director or Supervisory Board member of a number of subsidiary and affiliated companies, including: Pioneer First Polish Investment Fund, JSC, Pioneer Czech Investment Company and Pioneer Global Equity Fund PLC. From 1975 to 1984, Mr. Butler was a Vice-President of the National Association of Securities Dealers (currently Financial Industry Regulatory Authority). Mr. Butler has served as Trustee since theeach Fund’s inception and as Chairman of the Board for theeach Fund since 2006. Mr. Butler has also served as a member of the Audit Committee and Nominating Committee during his tenure as a Trustee for theeach Fund. In addition, since being appointed to the Board, Mr. Butler has further enhanced his experience and skills, in conjunction with the other Trustees, through the Board’s oversight of the Fund’sFunds’ officers in dealing with a diverse range of topics, to include but not limited to, portfolio management, legal and regulatory matters, compliance oversight, preparation of financial statements and oversight of the Fund’sFunds’ multiple service providers. The Board of Trustees, in its judgment of Mr. Butler’s professional experience in the financial services industry, including extensive involvement with international investing and as a trustee of closed-end investment companies, believes Mr. Butler contributes a diverse perspective to the Board.

Adam D. Crescenzi – Mr. Crescenzi is currently an Associate Trustee of Dean College and founding partner of Simply Tuscan Imports LLC. He currently serves as a Director of two non-profit organizations and as a member of the Board of Governors for the Naples Botanical Gardens and the Club Pelican Bay. Mr. Crescenzi graduated from the Greater Naples Leadership program in 2014. He previously served as a Trustee of Dean College from 2003 to 2015. He has been a founding partner and investor of several start-up technology and service firms, such as Telos Partners, a strategic business advisory firm, Creative Realties, Inc. a creative arts technology firm, and ICEX, Inc., whose principal business is web-based corporate exchange forums. Prior to being involved in multiple corporate start-ups, Mr. Crescenzi retired from CSC Index as Executive Vice-President of Management Consulting Services. During his career, Mr. Crescenzi has also served with various philanthropic organizations such as the Boston College McMullen Museum of Arts. Mr. Crescenzi has served as Trustee since theeach Fund’s inception.inception. Mr. Crescenzi has also served as a member of the Audit Committee and Nominating Committee during his tenure as a Trustee for theeach Fund. Mr. Crescenzi has served as Chairman of the Nominating Committee for theeach Fund since 2006. In addition, since being appointed to the Board, Mr. Crescenzi has further enhanced his experience and skills, in conjunction with the other Trustees, through the Board’s oversight of the Fund’sFunds’ officers in dealing with a diverse range of topics, to include but not limited to, portfolio management, legal and regulatory matters, compliance oversight, preparation of financial statements and oversight of the Fund’sFunds’ multiple service providers. The Board of Trustees, in its judgment of Mr. Crescenzi’s professional experience with emergent businesses, strategic consulting and as a trustee of closed-end investment companies, believes Mr. Crescenzi contributes a diverse perspective to the Board.

4

John F. Mee, Esquire– Mr. Mee has been a practicing attorney for over 40 years with experience in both Massachusetts’ state and Federal District Court. Mr. Mee continues to practice in the areas of commercial law, family law, product liability and criminal law. Mr. Mee is a member of the Bar of the Commonwealth of Massachusetts and the Middlesex and Central Middlesex Bar Associations, respectively. He was an instructor in the Harvard Law School Trial Advocacy Workshop from 1990 to 2009. During his legal career, Mr. Mee has also served as a director with various philanthropic organizations such as Holy Cross Alumni Association and the Concord Carlisle Scholarship Fund. Mr. Mee has served as Trustee since theeach Fund’s inception. Mr. Mee has also served as a member of the Audit Committee and Nominating Committee during his tenure as a Trustee for theeach Fund. In addition, since being appointed to the Board, Mr. Mee has further enhanced his experience and skills, in conjunction with the other Trustees, through the Board’s oversight of the Fund’sFunds’ officers in dealing with a diverse range of topics, to include but not limited to, portfolio management, legal and regulatory matters, compliance oversight, preparation of financial statements and oversight of the Fund’sFunds’ multiple service providers. The Board of Trustees, in its judgment of Mr. Mee’s professional experience as a reputable attorney and as a trustee of closed-end investment companies, believes Mr. Mee contributes a diverse perspective to the Board.

Richard C. Rantzow– Mr. Rantzow, a Certified Public Accountant, has over 40 years of experience in the finance industry and has served in a variety of roles. Mr. Rantzow during his nearly 30 year career at Ernst & Young, an independent public accounting firm, served as an audit partner and office managing partner. At Ernst & Young, he was responsible for the auditing of financial statements for a variety of companies, which included financial institutions. In addition, Mr. Rantzow also currently serves as Trustee and Audit Committee Chairman of the Liberty All-Star Equity Fund and Director and Audit Committee Chairman of the Liberty All-Star Growth Fund, each a closed-end investment company. Mr. Rantzow has served as Trustee since theeach Fund’s inception. Mr. Rantzow has also served as Chairman of the Audit Committee and as a member of the Nominating Committee during his tenure as a Trustee for theeach Fund. In addition, since being appointed to the Board, Mr. Rantzow has further enhanced his experience and skills, in conjunction with the other Trustees, through the Board’s oversight of the Fund’sFunds’ officers in dealing with a diverse range of topics, to include but not limited to, portfolio management, legal and regulatory matters, compliance oversight, preparation of financial statements and oversight of the Fund’sFunds’ multiple service providers. The Board of Trustees, in its judgment of Mr. Rantzow’s professional experience in the preparation and auditing of financial statements for financial institutions and as a trustee of closed-end investment companies, believes Mr. Rantzow contributes a diverse perspective to the Board.

Jerry G. Rutledge – Mr. Rutledge is the President and owner of Rutledge’s Inc., a retail clothing business that has operated for over 40 years. As a recognized community leader in the state of Colorado, Mr. Rutledge was elected as a Regent at the University of Colorado in 1994 and retired in 2007. In addition, Mr. Rutledge is currently serving as a Director of the University of Colorado Hospital and is a Trustee of Financial Investors Trust, an open-end investment company, and the Principal Real Estate Income Fund, a closed-end investment company. Mr. Rutledge also served as a Director of the American National Bank until 2009. Mr. Rutledge has served as Trustee since theeach Fund’s inception. Mr. Rutledge has also served as a member of the Audit Committee and Nominating Committee during his tenure as a Trustee for theeach Fund. Mr. Rutledge has further enhanced his experience and skills, in conjunction with the other Trustees, through the Board’s oversight of the Fund’sFunds’ officers in dealing with a diverse range of topics, to include but not limited to, portfolio management, legal and regulatory matters, compliance oversight, preparation of financial statements and oversight of the Fund’sFunds’ multiple service providers. The Board of Trustees, in its judgment of Mr. Rutledge’s leadership, long-term professional success in operating a business in a competitive industry and as a trustee of closed-end investment companies, believes Mr. Rutledge contributes a diverse perspective to the Board.

5

Hon. Vincent W. Versaci – Judge Versaci has served as a Judge and Supreme Court Justice in the State of New York since January 2003. Currently, Judge Versaci is assigned as an Acting Supreme Court Justice and also presides over the Surrogate’sSurrogate's Court for Schenectady County, New York. Previously, Judge Versaci has served as an Adjunct Professor at Schenectady County Community College and a practicing attorney with an emphasis on civil and criminal litigation primarily in New York State Courts. Judge Versaci has served as a member of theeach Fund’s Audit Committee, Nominating Committee and as a Trustee since March 2013. In addition, since being appointed to the Board, Judge Versaci has further enhanced his experience and skills, in conjunction with the other Trustees, through the Board’s oversight of the Fund’sFunds’ officers in dealing with a diverse range of topics, to include but not limited to, portfolio management, legal and regulatory matters, compliance oversight, preparation of financial statements and oversight of the Fund’sFunds’ multiple service providers. The Board of Trustees, in its judgment of Judge Versaci’s professional experience as a reputable attorney and judge, believes Judge Versaci contributes a diverse perspective to the Board.

Edmund J. Burke– Mr. Burke joined ALPS Fund Services, Inc.(“ALPS”) in 1991 and is currently the Chief Executive Officer and President of ALPS Holdings, Inc. (a wholly-owned subsidiary of DST Systems, Inc. (“DST”)), and a Director of ALPS Advisors, Inc., ALPS Distributors, Inc., ALPS Fund Services, Inc., and ALPS Portfolio Solutions Distributor, Inc. These organizations specialize in the day-to-day operations associated with both open- and closed-end investment companies, exchange traded funds and hedge funds. In addition, Mr. Burke is also currently Trustee, Chairman and President of the Financial Investors Trust, an open-end investment company, Trustee and President of Clough Funds Trust, an open-end investment company, and Trustee and Vice-President of the Liberty All-Star Equity Fund and Director and Vice President of the Liberty All-Star Growth Fund, Inc., each a closed-end investment company. Additionally, Mr. Burke is on the Board of Directors of Boston Financial Data Services, Inc., a financial services solutions provider. Mr. Burke has served as Trustee for theeach Fund since 2006 and as an interested trustee he does not serve as a member of the Audit and Nominating Committees. In addition, since being appointed to the Board, Mr. Burke has further enhanced his experience and skills, in conjunction with the other Trustees, through the Board’s oversight of the Fund’sFunds’ officers in dealing with a diverse range of topics, to include but not limited to, portfolio management, legal and regulatory matters, compliance oversight, preparation of financial statements and oversight of the Fund’sFunds’ multiple service providers. The Board of Trustees, in its judgment of Mr. Burke’s long-term professional experience with operational requirements and obligations in operating closed-end investment companies and as a trustee of closed-end investment companies, believes Mr. Burke contributes a diverse perspective to the Board.

6

James E. Canty, Esquire– Mr. Canty is a founding partner, President and Portfolio Manager for Clough Capital Partners, LP (“Clough”). Prior to founding Clough in 2000, Mr. Canty worked as a corporate and securities lawyer and Director of Investor Relations for Converse, Inc. from 1995 to 2000. He was a corporate and securities lawyer for the Boston offices of Goldstein & Manello, P.C. from 1993 to 1995 and Bingham, Dana and Gould from 1990 to 1993. Mr. Canty served as an Adjunct Professor at Northeastern University from 1996 to 2000. Mr. Canty is currently a Trustee of Clough Funds Trust and a member of the Board of Directors of Clough Offshore Fund, Ltd. and Clough Offshore Fund (QP), Ltd. Mr. Canty is also currently a Trustee of St. Bonaventure University, and serves on the boards of directors of Blacklight Power, Inc. and Razia’s Ray of Hope, a nonprofit organization. Mr. Canty has served as Trustee since theeach Fund’s inception and as an interested trustee does not serve as a member of the Audit and Nominating Committees. In addition, since being appointed to the Board, Mr. Canty has further enhanced his experience and skills, in conjunction with the other Trustees, through the Board’s oversight of the Fund’sFunds’ officers in dealing with a diverse range of topics, to include but not limited to, portfolio management, legal and regulatory matters, compliance oversight, preparation of financial statements and oversight of the Fund’sFunds’ multiple service providers. Mr. Canty is also a certified public accountant. The Board of Trustees, in its judgment of Mr. Canty’s long-term professional experience with portfolio management and as a trustee of closed-end investment companies, believes Mr. Canty contributes a diverse perspective to the Board.

Also, additional information regarding each Trustee’s current age, principal occupations and other directorships, if any, that have been held by the Trustees is provided in the table below.

Additional Information About Each about each Trustee/Nominee and Trustee and the Fund’s Officers

The table below sets forth the names, addresses and years of birth of the nominees, Trustees and principal officers of the Fund,Funds, the year each was first elected or appointed to office, their term of office, their principal business occupations during at least the last five years, the number of portfolios overseen by each Trustee of the Fund Complex and their other directorships of public companies.

7

Name, Address1 and Year of Birth | Position(s) Held with the Funds | Term of office and length of service with | Principal Occupation(s) During Past Five Years | Number of Portfolios in Fund Complex Overseen by Trustee | Other Directorships Held by Trustee During the Past Five Years |

| Non-Interested Trustees/Nominees | |||||

Robert L. Butler 1941 | Chairman of the Board and Trustee Nominee for: GLQ | Trustee since: GLV: 2004 GLQ: 2005 GLO: 2006 Term expires: GLQ: 2019 (if elected) GLO: 2017 | Since 2001, Mr. Butler has been an independent consultant for businesses. Mr. Butler has over 45 years experience in the investment business, including 17 years as a senior executive with a global investment management/natural resources company and 20 years with a securities industry regulation organization, neither of which Mr. Butler has been employed by since 2001. | 3 | None |

Adam D. Crescenzi 1942 | Trustee Nominee for: | Trustee since: GLV: 2004 GLQ: 2005 GLO: 2006 Term expires: GLQ: 2018 GLO: 2019 (if elected) | Mr. Crescenzi has served as the Founding Partner of Simply Tuscan Imports LLC since 2007. He has been a founder and investor of several start-up technology and service firms. . He currently serves as an Associate Trustee of Dean College and previously served as a Trustee from 2003 to 2015. He also serves as a Director of two non-profit organizations and as a member of the Board of Governors for the Naples Botanical Gardens and the Club Pelican Bay. He retired from CSC Index as Executive Vice-President of Management Consulting Services. | 3 | None |

John F. Mee 1943 | Trustee Nominee for: GLV | Trustee since: GLV: 2004 GLQ: 2005 GLO: 2006 Term expires: GLV: 2019 (if elected) GLQ: 2017 GLO: 2018 | Mr. Mee is an attorney practicing commercial law, family law, product liability and criminal law. Mr. Mee is currently a member of the Bar of the Commonwealth of Massachusetts. He serves on the Board of Directors of The College of the Holy Cross Alumni Association and Concord Carlisle Scholarship Fund, a Charitable Trust. Mr. Mee was from 1990 to 2009 an Advisor at the Harvard Law School Trial Advocacy Workshop. | 3 | None |

Name, Address1 and Year of Birth | Position(s) Held with the Funds | Term of office and length of service with | Principal Occupation(s) During Past Five Years | Number of Portfolios in Fund Complex Overseen by Trustee | Other Directorships Held by Trustee During the Past Five Years |

Richard C. Rantzow 1938 | Vice Chairman of the Board and Trustee Nominee for: GLQ | Trustee since: GLV: 2004 GLQ: 2005 GLO: 2006 Term expires: GLQ: 2019 (if elected) GLO: 2017 | Mr. Rantzow has over 40 years experience in the financial industry. His professional experience includes serving as an audit partner with Ernst & Young which specifically involved auditing financial institutions. Mr. Rantzow has also served in several executive positions in both financial and non-financial industries. Mr. Rantzow’s educational background is in accounting and he is a Certified Public Accountant who has continued to serve on several audit committees of various financial organizations. | 3 | Mr. Rantzow is a Trustee and Chairman of the Audit Committee of the Liberty All-Star Equity Fund and Director and Chairman of the Audit Committee of the Liberty All-Star Growth Fund, Inc. |

Jerry G. Rutledge 1944 | Trustee Nominee for: | Trustee since: GLV: 2004 GLQ: 2005 GLO: 2006 Term expires: GLQ: 2018 GLO: 2019 (if elected) | Mr. Rutledge is the President and owner of Rutledge’s Inc., a retail clothing business. Mr. Rutledge was from 1994 to 2007 a Regent of the University of Colorado. In addition, Mr. Rutledge is currently serving as a Director of the University of Colorado Hospital. Mr. Rutledge also served as a Director of the American National Bank from 1985 to 2009. | 4 | Mr. Rutledge is currently a Trustee of the Financial Investors Trust and the Principal Real Estate Income Fund. |

Hon. Vincent W. Versaci 1971 | Trustee Nominee for: GLV, GLQ and GLO | Trustee since: GLV: 2013 GLQ: 2013 GLO: 2013 Term GLQ: 2017 GLO: 2018 | Judge Versaci has served as a Judge in the New York State Courts since January 2003. Currently, Judge Versaci is assigned as an Acting Supreme Court Justice and also presides over the | 3 |

Name, Address1 and Year of Birth | Position(s) Held with the Funds | Term of office and length of service with | Principal Occupation(s) During Past Five Years | Number of Portfolios in Fund Complex Overseen by Trustee | Other Directorships Held by Trustee During the Past Five Years |

Interested Trustees | |||||

Edmund J. Burke 1961 | Trustee and President Nominee for: GLO | Trustee since: GLV: 2006 GLQ: 2006 GLO: 2006 Term expires: GLV: 2019 (if elected) GLQ: 2017 GLO: 2018 President since: GLV: 2004 GLQ: 2005 GLO: 2006 | Mr. Burke joined ALPS in 1991 and is currently the Chief Executive Officer and President of ALPS Holdings, Inc. | Mr. Burke is also Trustee, Chairman and President of Financial Investors | |

James E. Canty 1962 Clough Capital Partners, LP One Post Office Square 40th Floor Boston, MA 02109 | Trustee Nominee for: GLQ | Trustee since: GLQ: 2016 GLO: 2006 Term expires: GLQ: 2019 (if elected) GLO: 2017 | Mr. Canty is a founding partner, President and Portfolio Manager for Clough. Mr. Canty is deemed an affiliate of | ||

| Officers | |||||

Jeremy O. May 1970 | Treasurer | Officer since GLV: 2004 GLQ: 2005 GLO: 2006 | Mr. May joined ALPS in 1995 and is currently President of ALPS and ALPS Distributors, Inc., and Executive Vice President and Director of ALPS Advisors, Inc. and ALPS Holdings, Inc. Mr. May is also Director of ALPS Portfolio Solutions Distributor, Inc. Mr. May is deemed to be an affiliate of | N/A | N/A |

| Secretary | Officer since GLQ: 2015 GLO: 2015 | Ms. | N/A | N/A | |

| Chief Compliance Officer | Officer since GLQ: 2016 GLO: 2016 | ||||

| N/A | N/A | ||||

11

Alan Gattis 1980 | Assistant Treasurer | Officer since9: GLV: 2016 GLQ: 2016 GLO: 2016 | Mr. Gattis joined ALPS in 2011, and is currently Vice President and Fund Controller. Prior to ALPS Mr. Gattis served as | N/A | N/A |

| Jennifer A. Craig | Assistant Secretary | Officer since9: GLV: 2016 GLQ: 2016 GLO: 2016 | Ms. Craig joined ALPS in 2007 and is currently Assistant Vice President and Legal Manager of ALPS. Prior to joining ALPS, Ms. | N/A | N/A |

| 1 | Address: 1290 Broadway, Suite 1100, Denver, Colorado 80203, unless otherwise noted. |

| 2 | GLV commenced operations on July 28, 2004. |

| 3 | GLQ commenced operations on April 27, 2005. |

| GLO commenced operations on April 25, 2006. |

| 5 | The Fund Complex for all Trustees, except Mr. Rutledge, Mr. Canty and Mr. Burke, consists of the Clough Global Allocation Fund, Clough Global Equity Fund and Clough Global Opportunities Fund. The Fund Complex for Mr. Rutledge |

| “Interested Trustees” refers to those Trustees who constitute “interested persons” of |

| Mr. Burke is considered to be an “Interested Trustee” because he is President of |

| Mr. Canty is considered to be an “Interested Trustee” because of his affiliation with Clough, which acts as |

| Officers are elected annually and each officer will hold such office until a successor has been elected by the Board. |

12

Beneficial Ownership Ofof GLV Common Shares, GLQ Common Shares and GLO Common Shares Held Inin the Fund And In All Funds In The Family Of Investment Companies For Each Trustee And Complex by each Trustee/Nominee For Election As Trustee

Set forth in the table below is the dollar range of equity securities held in theeach Fund and on an aggregate basis for all Funds overseen in a familythe entire Family of investment companiesInvestment Companies overseen by each Trustee.

| Independent Trustee/Nominee | Dollar Range1 of Equity Securities Held in GLV: | Dollar Range1 of Equity Securities Held in GLQ: | Dollar Range1 of Equity Securities Held in GLO: | Aggregate Dollar Range of Equity Securities Held in the Family of Investment Companies |

| Robert L. Butler | $10,001-$50,000 | $10,001-$50,000 | $10,001-$50,000 | $50,001-$100,000 |

| Adam D. Crescenzi | $0 | $0 | $1-$10,000 | $1-$10,000 |

| John F. Mee | $0 | $0 | $0 | $0 |

| Richard C. Rantzow | $10,001-$50,000 | $1-$10,000 | $0 | $10,001-$50,000 |

| Jerry G. Rutledge | Over $100,000 | Over $100,000 | $50,001-$100,000 | Over $100,000 |

| Vincent W. Versaci | $1-$10,000 | $1-$10,000 | $1-$10,000 | $10,001-$50,000 |

| Interested Trustee/Nominee | ||||

| Edmund J. Burke | $0 | $0 | $0 | $0 |

| James E. Canty | Over $100,000 | Over $100,000 | Over $100,000 | Over $100,000 |

| This information has been furnished by each Trustee and nominee for election as Trustee as of March 31, |

| Ownership amount constitutes less than 1% of the total |

| The Funds in the family of investment companies for all Trustees, consists of the Clough Global Allocation Fund, Clough Global Equity Fund and Clough Global Opportunities Fund. |

As of March 31, 2015,2016, none of the independent trustees, meaning those Trustees who are not “interested persons” as such term is defined byin Section 2(a)(19) of the 1940 Act and are independent under the NYSE MKT LLC’s (“NYSE MKT”MKT”) listing standardsListing Standards (each an “Independent Trustee”“Independent Trustee” and collectively the “Independent Trustees”“Independent Trustees”), nor members of their immediate families owned securities, beneficially or of record, in Clough Capital L.P. (the “Adviser” or “Clough”), or an affiliate or person directly or indirectly controlling, controlled by, or under common control with Clough.the Adviser, other than investments in the Funds and investments in affiliated investment vehicles that, pursuant to guidance from the SEC Staff, do not affect such Trustee’s independence. Furthermore, over the past five years, neither the Independent Trustees nor members of their immediate families have had any direct or indirect interest, the value of which exceeds $120,000, in Cloughthe Adviser or any of its affiliates. In addition, since the beginning of the last two fiscal years, neither the Independent Trustees nor members of their immediate families have conducted any transactions (or series of transactions) or maintained any direct or indirect relationship in which the amount involved exceeds $120,000 and to which Cloughthe Adviser or any affiliate of Cloughthe Adviser was a party.

13

Trustee Compensation

The following table sets forth certain information regarding the compensation of the Fund’sFunds’ Trustees for the twelve-monthsfiscal year ended October 31, 2014.2015. Trustees and Officers of the FundFunds who are employed by ALPS or Clough receive no compensation or expense reimbursement from the Fund.Funds.

| Aggregate Compensation Paid From | Total Compensation From the Fund and Fund Complex Paid to Trustees** | |

| Name of Trustee/Nominee | Clough Global Equity Fund* | |

| Edmund J. Burke | None | None |

| Robert L. Butler | $24,000 | $72,000 |

| James E. Canty | None | None |

| Adam D. Crescenzi | $20,000 | $60,000 |

| John F. Mee | $20,000 | $60,000 |

| Richard C. Rantzow | $22,000 | $66,000 |

| Jerry G. Rutledge | $20,000 | $102,000 |

| Vincent W. Versaci | $20,000 | $60,000 |

| Total | $126,000 | $420,000 |

Compensation Table for the Fiscal Year Ended October 31, 2015.

| Name of Trustee/ Nominee | Clough Global Allocation Fund | Clough Global Equity Fund | Clough Global Opportunities Fund | Total Compensation Paid From the Fund Complex1 |

| Robert L. Butler | $28,600 | $32,200 | $28,600 | $89,400 |

| Adam D. Crescenzi | $23,833 | $26,833 | $23,833 | $74,500 |

| John F. Mee | $23,833 | $26,833 | $23,833 | $74,500 |

| Richard C. Rantzow | $26,217 | $29,517 | $26,217 | $81,950 |

| Jerry G. Rutledge | $23,833 | $26,833 | $23,833 | $75,059 |

| Vincent W. Versaci | $23,833 | $26,833 | $23,833 | $74,500 |

14

During the fiscal year ended MarchOctober 31, 2014,2015, the Board of the FundGLV and GLO met four times. In September 2014, the Fund changed its fiscal year end to October 31. During the period April 1, 2014 to October 31, 2014,seven times and the Board of the FundGLQ met twonine times. Each Trustee then serving in such capacity attended at least 75% of the meetings of Trustees and of any Committee of which he is a member.

Leadership Structure of the Board of Trustees

The Board, which has overall responsibility for the oversight of theeach Fund’s investment programs and business affairs, has appointed an Independent Trustee as Chairman of the Board whose role is to preside at all meetings of the Board. The Board has also appointed an Independent Trustee as Vice-Chairman of the Fund.Funds. The Chairman is involved, at his discretion, in the preparation of the agendas for the Board meetings. In between meetings of the Board, the Chairman may act as liaison between the Board and the Fund’sFunds’ officers, attorneys and various other service providers, including but not limited to, the Fund’sFunds’ investment adviser, administrator and other such third parties servicing the Fund.Funds. The Chairman may also perform other functions as may be delegated by the Board from time to time. The Board believes that the use of an Independent Trustee as Chairman is the appropriate leadership structure for mitigating potential conflicts of interest associated with appointing an Interested Trustee as chairman and facilitates the ability to maintain a robust culture of compliance.compliance. The Board has three standing committees, each of which enhances the leadership structure of the Board: the Audit Committee; the Nominating Committee; and the Executive Committee. The Audit Committee and Nominating Committee are each chaired by, and composed of, members who are Independent Trustees. The Executive Committee consists of two Interested Trustees and one Independent Trustee.

Oversight of Risk Management

However, as required under the 1940 Act, the Board has adopted on the Fund’sFunds’ behalf a vigorous risk program that mandates the Fund’sFunds’ various service providers, including the investment adviser, to adopt a variety of processes, procedures and controls to identify various risks, mitigate the likelihood of such adverse events from occurring and/or attempt to limit the effects of such adverse events on thea Fund. The Board fulfills its leadership role by receiving a variety of quarterly written reports prepared by the Fund’sFunds’ Chief Compliance Officer (“CCO”) that: (i) evaluate the operation of the Fund’sFunds’ service providers; (ii) make known any material changes to the policies and procedures adopted by the FundFunds or itstheir service providers since the CCO’s last report and; (iii) disclose any material compliance matter that occurred since the date of the last CCO report. In addition, the Chairman and the Independent Trustees meet quarterly in executive sessions without the presence of any Interested Trustees, the investment adviser, the administrator, or any of their affiliates. This configuration permits the Chairman and the Independent Trustees to effectively receive the information and have private discussions necessary to perform its risk oversight role, exercise independent judgment, and allocate areas or responsibility between the full Board, its various committees and certain officers of the Fund.Funds. Furthermore the Independent Trustees have engaged independent legal counsel and auditors to assist the Independent Trustees in performing their responsibilities. As discussed above and in consideration of other factors not referenced herein, the function of the Board with respect to its leadership role concerning risk management is one of oversight and not active management or coordination of the Fund’sFunds’ day-to-day risk management activities.

15

The role of the Fund’sFunds’ Audit Committee is to assist the Board in its oversight of: (i) the quality and integrity of Fund’sFunds’ financial statements, reporting process and the independent registered public accounting firm (the “independent accountant”) and reviews thereof; (ii) the Fund’sFunds’ accounting and financial reporting policies and practices, its internal controls and, as appropriate, the internal controls of certain service providers; (iii) the Fund’sFunds’ compliance with legal and regulatory requirements; and (iv) the independent accountant’s qualifications, independence and performance. The Audit Committee is also required to prepare an audit committee report pursuant to the rules of the SEC for inclusion in theeach Fund’s annual proxy statement. TheEach Audit Committee operates pursuant to an Audit Committee Charter (the “Charter”“Charter”) that was most recently reviewed and approved by the Audit Committee on December 3, 2014.23, 2015. The Charter is available at the Fund’sFunds’ website, www.cloughglobal.com. As set forth in the Charter, management is responsible for maintaining appropriate systems for accounting and internal control and the Fund’sFunds’ independent accountant is responsible for planning and carrying out proper audits and reviews. The independent accountant is ultimately accountable to theeach Fund’s Board and Audit Committee, as representatives of theeach Fund’s shareholders. The independent accountant for the FundFunds reports directly to the Audit Committee.

In performing its oversight function, at a meeting held on December 23, 2014,2015, the Audit Committee reviewed and discussed with management of the FundFunds and the independent accountant, Cohen Fund Audit Services, Ltd. (“Cohen”Cohen”), the audited financial statements of the FundFunds as of and for the fiscal year ended October 31, 2014,2015, and discussed the audit of such financial statements with the independent accountant.

In addition, the Audit Committee discussed with the independent accountant the accounting principles applied by the FundFunds and such other matters brought to the attention of the Audit Committee by the independent accountant required by the Public Company Accounting Oversight Board (“PCAOB”) Audit Standard No. 16 Communications with Audit Committees. The Audit Committee also received from the independent accountant the written disclosures and letters required by PCAOB Rule 3526, Communication with Audit Committees Concerning Independence, and discussed the relationship between the independent accountant and the FundFunds and the impact that any such relationships might have on the objectivity and independence of the independent accountant.

16

As set forth above, and as more fully set forth in the Charter, the Audit Committee has significant duties and powers in its oversight role with respect to theeach Fund’s financial reporting procedures, internal control systems and the independent audit process.

The members of the Audit Committees are not, and do not represent themselves to be, professionally engaged in the practice of auditing or accounting and are not employed by the FundFunds for accounting, financial management or internal control purposes. Moreover, theeach Audit Committee relies on and makes no independent verification of the facts presented to it or representations made by management or the independent verification of the facts presented to it or representation made by management or the Fund’sFunds’ independent accountant. Accordingly, the Audit Committee’s oversight does not provide an independent basis to determine that management has maintained appropriate accounting and/or financial reporting principles and policies, or internal controls and procedures designed to assure compliance with accounting standards and applicable laws and regulations. Furthermore, the Audit Committee’s considerations and discussions referred to above do not provide assurance that the audit of theeach Fund’s financial statements has been carried out in accordance with generally accepted accounting standards or that the financial statements are presented in accordance with generally accepted accounting principles.

Based on its consideration of the audited financial statements and the discussions referred to above with management and the Fund’sFunds’ independent accountant, and subject to the limitations on the responsibilities and role of the Audit Committee set forth in the Charter and those discussed above, theeach Audit Committee recommends that theeach Fund’s audited financial statements, subject to the modifications discussed at the December 23, 20142015 Audit Committee meeting, be included in the Fund’sFunds’ Annual Report for the fiscal year ended October 31, 2014.2015.

SUBMITTED BY THE AUDIT COMMITTEE OF THEEACH FUND’S BOARD OF TRUSTEES

Richard C. Rantzow, Chairman

Robert L. Butler

Adam D. Crescenzi

John F. Mee

Jerry G. Rutledge

Vincent W. Versaci

December 23, 20142015

Audit Committee

Based on the findings of the Audit Committee, the Audit Committee has determined that Mr. Richard C. Rantzow is theeach Fund’s “audit committee financial expert,” as defined in the rules promulgated by the SEC, and as required by NYSE MKT listing standards. Mr. Rantzow serves as the Chairman of the Audit Committee for theeach Fund.

17

Nominating Committee

When such vacancies or creations occur, the Nominating Committee will consider Trustee candidates recommended by a variety of sources to include theeach Fund’s respective shareholders. The Nominating Committee has a diversity policy. In considering Trustee candidates, the Nominating Committee will take into consideration the interest of shareholders, the needs of the Board and the Trustee candidate’s qualifications, which include but are not limited to, the diversity of the individual’s professional experience, education, individual qualification or skills.

Shareholders may submit for the Committee’s consideration recommendations regarding potential independent Board member nominees. Each eligible shareholder or shareholder group may submit no more than one independent Board member nominee each calendar year.

In order for the Committee to consider shareholder submissions, the following requirements must be satisfied regarding the nominee:

| (a) | The nominee must satisfy all qualifications provided under the Nominating Committee Charter and in the Fund’s organizational documents, including qualification as a possible independent Board member. |

| (b) | The nominee may not be the nominating shareholder, a member of the nominating shareholder group or a member of the immediate family of the nominating shareholder or any member of the nominating shareholder group. |

| (c) | Neither the nominee nor any member of the nominee’s immediate family may be currently employed or employed within the last year by any nominating shareholder entity or entity in a nominating shareholder group. |

| (d) | Neither the nominee nor any immediate family member of the nominee is permitted to have accepted directly or indirectly, during the year of the election for which the nominee’s name was submitted, during the immediately preceding calendar year, or during the year when the nominee’s name was submitted, any consulting, advisory, or other compensatory fee from the nominating shareholder or any member of a nominating shareholder group. |

18

| (e) | The nominee may not be an executive officer, Trustee (or person fulfilling similar functions) of the nominating shareholder or any member of the nominating shareholder group, or of an affiliate of the nominating shareholder or any such member of the nominating shareholder group. |

| (f) | The nominee may not control (as that term is defined under the 1940 Act) the nominating shareholder or any member of the nominating shareholder group (or, in the case of a holder or member that is a fund, an interested person of such holder or member as defined by Section 2(a)(19) of the 1940 Act). |

| (g) | A shareholder or shareholder group may not submit for consideration a nominee who has previously been considered by the Committee. |

In order for the Committee to consider shareholder submissions, the following requirements must be satisfied regarding the shareholder or shareholder group submitting the proposed nominee:

| (a) | Any shareholder or shareholder group submitting a proposed nominee must beneficially own, either individually or in the aggregate, more than 5% of the Fund’s securities that are eligible to vote both at the time of submission of the nominee and at the time of the Board member election. Each of the securities used for purposes of calculating this ownership must have been held continuously for at least two years as of the date of the nomination. In addition, such securities must continue to be held through the date of the meeting. The nominating shareholder or shareholder group must also bear the economic risk of the investment and the securities used for purposes of calculating the ownership cannot be held “short.” |

| (b) | The nominating shareholder or shareholder group must not qualify as an adverse holder. In other words, if such shareholder were required to report beneficial ownership of its securities, its report would be filed on Securities Exchange Act Schedule 13G instead of Schedule 13D in reliance on Securities Exchange Act Rule 13d-1(b) or (c). |

| (c) | Shareholders or shareholder groups submitting proposed nominees must substantiate compliance with the above requirements at the time of submitting their proposed nominee as part of their written submission to the attention of the Fund’s Secretary, which must include: (i) a brief description of the business desired to be brought before the annual or special meeting and the reasons for conducting such business at the annual or special meeting, (ii) the name and address, as they appear on the Fund’s books, of the shareholder proposing such business or nomination, (iii) a representation that the shareholder is a holder of record of stock of the Fund entitled to vote at such meeting and intends to appear in person or by proxy at the meeting to present such proposal or nomination; (iv) whether the shareholder plans to deliver or solicit proxies from other shareholders; (v) the class and number of shares of the capital stock of the Fund, which are beneficially owned by the shareholder and, if applicable, the proposed nominee to the Board of Trustees, (vi) any material interest of the shareholder or nominee in such business; (vii) to the extent to which such shareholder (including such shareholder’s principals) or the proposed nominee to the Board of Trustees has entered into any hedging transaction or other arrangement with the effect or intent of mitigating or otherwise managing profit, loss, or risk of changes in the value of the common stock or the daily quoted market price of the Fund held by such shareholder (including shareholder’s principals) or the proposed nominee, including independently verifiable information in support of the foregoing; and (viii) in the case of a nomination of any person for election as a Trustee, such other information regarding such nominee proposed by such shareholder as would be required to be included in a proxy statement filed pursuant to Regulation 14A under the Securities Exchange Act of 1934, as amended. |

19

It shall be in the Committee’s sole discretion whether to seek corrections of a deficient submission or to exclude a nominee from consideration.

Any shareholder recommendation described above must be sent to the applicable Fund’s Secretary c/o ALPS.

Executive Committee

The Executive Committee meets periodically to take action, as authorized by the Board, if the Board cannot meet. Members of the Executive Committee are currently Messrs. Burke, Butler and Canty. During the fiscal year ended MarchOctober 31, 2014,2015, the Executive Committee did not meet. In September 2014, the Fund changed its fiscal year end to October 31. During the period April 1, 2014 to October 31, 2014,of GLQ met four times, and the Executive Committee did not meet.Committees of both GLV and GLO, each met one time.

Compensation Committee

The Fund doesFunds do not have a compensation committee.

Other Board Related Matters

The Fund doesFunds do not require Trustees to attend the Annual Meeting of Shareholders. No Trustees attended the Fund’sFunds’ Annual Meeting of Shareholders held in 2014.2015.

Performance (annualized returns as of March 31, 2015)* | |||||

| Fund | Long/Short Fund Peer Group | Global Fund Peer Group | |||

| 1 Year | 6.3 | % | 4.1 | % | 1.4% |

| 3 Year | 11.4 | % | 10.6 | % | 8.4% |

| 5 Year | 8.8 | % | 8.7 | % | 7.1% |

REQUIRED VOTE

The election of each of the listed nominees for Trustee of thea Fund requires the affirmative vote of the holders of a plurality of the Common Shares entitled to vote andvotes cast by holders of each Fund represented at the Fund’s Meeting, if a quorum is present.

| Trustees and Executive Officers | ||

Name & Address1 | Percentage of Shares Held | Total Shares Owned |

GLV Common Shares2 | ||

| Edmund J. Burke* | 0% | 0 |

| Robert L. Butler | >1% | 2,007 |

| James E. Canty | >1% | 8,783 |

| Adam D. Crescenzi | 0% | 0 |

| Jeremy O. May* | 0% | 0 |

| John F. Mee | 0% | 0 |

| Richard C. Rantzow | >1% | 2,188 |

| Jerry G. Rutledge | >1% | 7,712 |

| Vincent W. Versaci | >1% | 320 |

| All Trustees and Executive Officers as a group | >1% | 21,010 |

GLQ Common Shares2 | ||

| Edmund J. Burke* | 0% | 0 |

| Robert L. Butler | >1% | 1,982 |

| James E. Canty | >1% | 105,887 |

| Adam D. Crescenzi | 0% | 0 |

| Jeremy O. May* | 0% | 0 |

| John F. Mee | 0% | 0 |

| Richard C. Rantzow | 0% | 24 |

| Jerry G. Rutledge | >1% | 12,750 |

| Vincent W. Versaci | >1% | 1,165 |

| All Trustees and Executive Officers as a group | >1% | 121,808 |

GLO Common Shares2 | ||

| Edmund J. Burke* | 0 | |

| Robert L. Butler | >1% | 1,857 |

21

| James E. Canty | >1% | 12,785 |

| Adam D. Crescenzi | >1% | 406 |

| Jeremy O. May* | 0% | 0 |

| John F. Mee | 0% | 0 |

| Richard C. Rantzow | 0% | 0 |

| Jerry G. Rutledge | >1% | 5,000 |

| Vincent W. Versaci | 0% | 390 |

| All Trustees and Executive Officers as a group | >1% | 20,438 |

* Mr. Burke is a Trustee and the Principal Executive Officer of each Fund. Mr. May is the Principal Financial Officer of each Fund.

GLV Common Shares3 | ||

Bank of America Corporation Bank of America Corporate Center 100 N Tryon Street Charlotte, NC 28255 | 5.74% | 596,399 |

Advisors Asset Management, Inc. 18925 Base Camp Road Monument, CO 80132 | 6.61% | 687,331 |

GLQ Common Shares3 | ||

Bank of America Corporation Bank of America Corporate Center 100 N Tryon Street Charlotte, NC 28255 | 7.86% | 1,387,304 |

RiverNorth Capital Management LLC 325 N. LaSalle Street Suite 645 Chicago, IL 60654-7030 | 8.97% | 1,584,239 |

GLO Common Shares3 | ||

Bank of America Corporation Bank of America Corporate Center 100 N Tryon Street Charlotte, NC 28255 | 6.78% | 3,495,803 |

RiverNorth Capital Management LLC 325 N. LaSalle Street Suite 645 Chicago, IL 60654-7030 | 7.88% | 4,061,636 |

(1) The address for each Trustee and/or Officer of each Fund is 1290 Broadway, Suite 1100, Denver, Colorado 80203, unless otherwise noted.

(2) The table above shows Trustees’ and Executive Officers’ ownership of Shares of each Fund as of March 31, 2016.

22” PROPOSAL 2.

(3) The table above shows 5% or greater shareholders’ ownership of Shares as of May 23, 2016. The information contained in this table is based on Schedule 13G filings made on or before May 23, 2016.

ADDITIONAL INFORMATION

Independent Registered Public Accounting Firm

Cohen Fund Audit Services, Ltd. (“Cohen”Cohen”), 1350 Euclid Avenue, Suite 800, Cleveland, OH 44115,44145, has been selected to serve as theeach Fund’s independent registered public accounting firm for theeach Fund’s fiscal year ending October 31, 2015.2016. Cohen acted as theeach Fund’s independent registered public accounting firm for the fiscal year ended October 31, 2014.2015. The Fund knowsFunds know of no direct financial or material indirect financial interest of Cohen in any of the Fund.Funds. A representative of Cohen will not be present at the Meeting,Meetings, but will be available by telephone and will have an opportunity to make a statement, if asked, and will be available to respond to appropriate questions.

Principal Accounting Fees and Services

The following table sets forth the aggregate audit and non-audit fees billed to theeach Fund for each of the last three fiscal years/periodsperiod for professional services rendered by the Fund’sFunds’ principal accountant, Cohen.

Fiscal period ended October 31, 2014 (1) | Fiscal year ended March 31, 2014 | Fiscal year ended March 31, 2013 | ||||

| Audit Fees (2) | $20,500 | $20,500 | $20,000 | |||

| Audit-Related Fees (3) | 0 | 0 | 0 | |||

| Tax Fees (4) | 3,000 | 3,000 | 3,000 | |||

| All Other Fees (5) | 0 | 0 | 0 | |||

| Aggregate Non-Audit Fees (6) | 3,000 | 3,000 | 3,000 | |||

Fiscal year ended October 31, 2015 | Fiscal period ended October 31, 2014 (1) | Fiscal year ended March 31, 2014 | |||||||

| GLV | GLQ | GLO | GLV | GLQ | GLV | GLV | GLQ | GLO | |

| Audit Fees (2) | $20,500 | $20,500 | $20,500 | $20,500 | $20,500 | $20,500 | $20,500 | $20,500 | $20,500 |

| Audit-Related Fees (3) | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Tax Fees (4) | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 |

| All Other Fees (5) | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Aggregate Non-Audit Fees (6) | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 |

| (1) | In 2014, |

| (2) | Audit Fees are fees billed for professional services rendered by Cohen for the audit of the Fund’s annual financial statements and for the services that are normally provided by Cohen in connection with the statutory and regulatory filings or engagements. |

| (3) | Audit-Related Fees are fees billed for assurance and related services by Cohen that are reasonably related to the performance of the audit of the Fund’s financial statements and are not reported under the caption “Audit Fees”. |

| (4) | Tax Fees are fees billed for professional services rendered by Cohen for tax compliance, tax advice and tax planning. In all periods shown in the table, such services consisted of preparation of |

23

| (5) | All Other Fees are fees billed for products and services provided by Cohen, other than the services reported under the captions “Audit Fees”, “Audit-Related Fees” and “Tax Fees”. |

| (6) | Aggregate Non-Audit Fees are non-audit fees billed by Cohen for services rendered to the Fund, the Fund’s investment adviser (the “Adviser”) and any entity controlling, controlled by or under common control with the Adviser that provides ongoing services to the registrant (collectively, the “Covered Entities”). The Aggregate Non-Audit Fee includes the Tax Fees disclosed pursuant to Footnote 4 above. During all periods shown in the table, no portion of such fees related to services rendered by Cohen to the Adviser or any other Covered Entity. |

Other Methods of Proxy Solicitation

In addition to the solicitation of proxies by internet or mail, officers of the Funds and officers and regular employees of DST Systems, Inc. (“DST”), the Funds’ transfer agent, ALPS Fund Services, Inc. (“ALPS”), the Funds’ administrator, and affiliates of DST, ALPS or other representatives of the Funds may also solicit proxies by telephone, internet or in person. The expenses incurred in connection with preparing the Proxy Statement and its enclosures will be paid by the Funds. The Funds will also reimburse brokerage firms and others for their expenses in forwarding solicitation materials to the beneficial owners of the Funds’ Shares (as defined below). In addition, the Funds have engaged Boston Financial Data Services, Inc. (“BFDS”) to assist in the proxy effort for the Funds. Under the terms of the engagement, BFDS will be providing a web site for the dissemination of these proxy materials and tabulation services.

24

The Investment Adviser and Administrator

Clough is the investment adviser for each of the Fund,Funds, and its business address is One Post Office Square, 40th40th Floor, Boston, Massachusetts 02109.

ALPS is the administrator for theeach Fund, and its business address is 1290 Broadway, Suite 1100, Denver, Colorado 80203.

Section 16(a) Beneficial Ownership Reporting Compliance

Section 16(a) of the 1934 Act and Section 30(h) of the 1940 Act, and the rules thereunder, require the Fund’sFunds’ officers and Trustees, officers and directors of the investment adviser, affiliated persons of the investment adviser, and persons who beneficially own more than 10% of a registered class of thea Fund’s Common Shares (the “Reporting Persons”) to file reports of ownership and changes in ownership with the SEC and the NYSE MKT and to furnish the FundFunds with copies of all Section 16(a) forms they file. Based solely on these reports and other information provided to the FundFunds by the Reporting Persons, theeach Fund believes that all Reporting Persons timely filed the required reports during fiscal year ended October 31, 2014.

2015.Broker Non-Votes and Abstentions

The affirmative vote of a plurality of votes cast for each nominee by the holders entitled to vote for a particular nominee is necessary for the election of a nominee.

For the purpose of electing nominees, abstentions or broker non-votes will not be counted as votes cast and will have no effect on the result of the election. Abstentions or broker non-votes, however, will be considered to be present at the Meeting for purposes of determining the existence of each Fund’s quorum.

Shareholders of each Fund will be informed of the voting results of the Meeting in the Funds’ Annual Report dated October 31, 2016.

OTHER MATTERS TO COME BEFORE THE MEETING

The Trustees of theeach Fund do not intend to present any other business at the Meeting.Meeting, nor are they aware that any shareholder intends to do so. If, however, any other matters, including adjournments, are properly brought before athe Meeting, the persons named in the accompanying form of proxy will vote thereon in accordance with their judgment.

Shareholder Communications with Board of Trustees

Shareholders may mail written communications to theeach Fund’s Board, to committees of the Board or to specified individual Trustees in care of the Secretary of the Fund,Funds, 1290 Broadway, Suite 1100, Denver, Colorado 80203. All shareholder communications received by the Secretary will be forwarded promptly to the applicable Board, the relevant Board’s committee or the specified individual Trustees, as applicable, except that the Secretary may, in good faith, determine that a shareholder communication should not be so forwarded if it does not reasonably relate to thea Fund or its operations, management, activities, policies, service providers, Board, officers, shareholders or other matters relating to an investment in thea Fund or is purely ministerial in nature.

25

SHAREHOLDER PROPOSALS

Any shareholder proposal to be considered for inclusion in the Fund’sFunds’ proxy statement and form of proxy for the annual meeting of shareholders to be held in 20152016 should have been received by the Secretary of the relevant Fund no later than January 29, 2015.March 3, 2016. To submit a shareholder proposal for a Fund’s annual meeting, a shareholder is required to five to a Fund notice of, and specified information with respect to any proposals pursuant to Rule 14a-8 under the 1934 Act by February 20, 2017. In addition, pursuant to theeach Fund’s By-Laws, a shareholder is required to give to thea Fund notice of, and specified information with respect to, any proposals that such shareholder intends to present at the 20162017 annual meeting nonot later than the close of business on the ninetieth (120th) day, nor earlier than January 31, 2016, and no later than March 1, 2016.the close of business on the one hundred twentieth (150th) day, prior to the first anniversary of the preceding year’s annual meeting. Under the circumstances described in, and upon compliance with, Rule 14a-4(c) under the 1934 Act, thea Fund may solicit proxies in connection with the 20162017 annual meeting which confer discretionary authority to vote on any shareholder proposals of which the Secretary of the relevant Fund does not receive notice in accordance with the aforementioned date. Timely submission of a proposal does not guarantee that such proposal will be included.

HOUSEHOLDING OF PROXY MATERIALS

Shareholders who share the same address and last name may receive only one copy of the proxy materials unless Boston Financial Data Services, Inc. (“BFDS”),BFDS, in the case of shareholders of record, or such shareholder’sshareholder's broker, bank or nominee, in the case of shareholders whose shares are held in street name, has received contrary instructions. This practice, known as “householding,” is designed to reduce printing and mailing costs. Shareholders desiring to discontinue householding and receive a separate copy of the proxy materials, may (1) if their shares are held in street name, notify their broker, bank or nominee or (2) if they are shareholders of record, direct a written request to BFDS.

IF VOTING BY PAPER PROXIES, IT IS IMPORTANT THAT PROXIES BE RETURNED PROMPTLY. SHAREHOLDERS WHO DO NOT EXPECT TO ATTEND THEA MEETING ARE THEREFORE URGED TO COMPLETE, SIGN, DATE, AND RETURN THE PROXY CARD AS SOON AS POSSIBLE IN THE ENCLOSED POSTAGE-PAID ENVELOPE.

26

27

[INTENTIONALLY LEFT BLANK]

28